by Jeff Clark

Senior Precious Metals Analyst

July 13, 2012

from

CaseyResearch Website

Doug Casey told me in January,

"The only thing that scares me is that

central banks are buying a lot of gold; they're historically contrary

indicators."

When it comes to buying gold, central banks have

such a poor timing record that they're frequently joked about as a contrary

indicator.

We dislike referring to tonnes of gold instead of ounces. Gold is priced by

the ounce. But certain market players, especially central banks, report gold

transactions in tonnes. One metric ton (tonne) equals 32,150.7 troy ounces.

Recently, they have been buying, quite literally, tonnes of it.

Consider the following:

-

Net central-bank purchases in 2011

exceeded 455 tonnes. This was only the second increase since 1988

(the first in 2010) and the largest since 1964.

-

Turkey has added over 123 tonnes since

last October, buying 29.7 tonnes in April alone.

-

Mexico has purchased over 100 tonnes

since February 2011.

-

The Philippines added 32 tonnes in

March, its second-largest monthly purchase ever. Largely under the

radar is the fact that it's buying some of its local production.

-

Russia continues buying, adding 15.5

tonnes in May. Its total reserves now stand at 911.3 tonnes, the

highest level since 1993.

-

Thailand has raised its holdings by more

than 80% since mid-2010.

-

South Korea has bought 40 tonnes since

May 2009, an increase of 180%.

-

The World Gold Council (WGC) reported

that central-bank purchases totaled 80.8 tonnes in Q1 2012, about 7%

of global demand.

-

Over the past 12 months, net purchases

have averaged almost 20% of total annual supply.

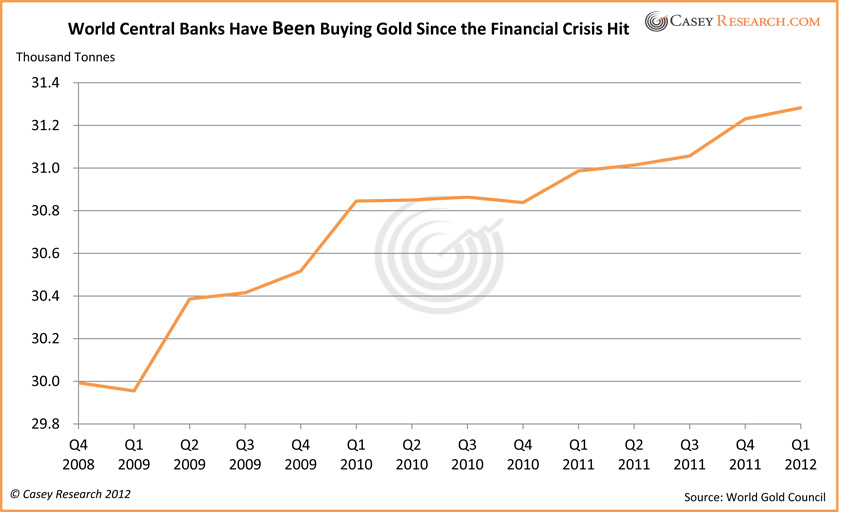

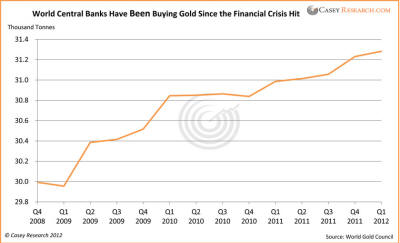

Here's the picture of what has transpired since

the financial crisis hit in late 2008.

Central banks have added a net of 1,290 tonnes

since the fourth quarter of 2008.

This total excludes China and other nations that

don't regularly report their activity, as well as countries that have been

surreptitiously buying their own production.

That's a lot of gold buying. One has to wonder whether so much buying may in

fact signal a top for gold. After all, a number of prominent analysts have

claimed for some time that gold is in a bubble and that it's all downhill

from here.

Not so fast. Like many mainstream reports, looking at the short-term picture

usually leads to erroneous conclusions. Let's put central-bank purchases

into historical perspective.

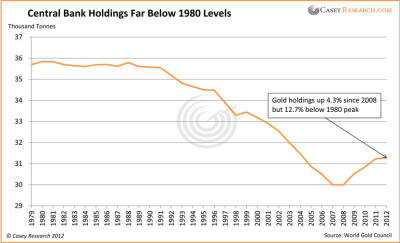

In spite of the recent activity, world

central-bank holdings are far below what they were in 1980. Clearly, a few

years of net buying does not a bubble make.

The difference is greater than you might realize.

Consider that since 1980…

-

The global population has grown 55%

-

Worldwide gold supply has grown 120%

-

Foreign-exchange holdings have increased

650% since 1995, and now total $10.4 trillion

It seems rather obvious that a lot more

"catch-up" buying is needed before we start talking about a top for gold on

this basis.

Meanwhile, we think the trend of central-bank gold buying will continue.

It's not hard to see why: central bankers around the world know what it must

ultimately mean to run the printing presses the way the US has since 2008,

even if price inflation is not immediately obvious.

It's no surprise that they want to hedge their

bets, moving more reserves into something with actual value... something

that can't be debased with a few keystrokes. The US dollar has been the

world's reserve currency since WWII, and that's beginning to change - the

movement into gold is just one facet of that change.

The entire world may indeed be beginning to understand that it's operating

on a fiat currency system backed by nothing. At the same time, the sovereign

debt crisis in the Eurozone is intensifying, and some countries have

succeeded in inflating their currencies faster than

the FED has inflated the

USD.

It doesn't take Nostradamus to read this writing

on the wall… and while the world's central bankers can lie to the public,

they themselves know how bad things are.

In fact,

the WGC is so confident that central banks will continue to buy

gold that it's changed its reporting structure: it's added "official sector

purchases" as a new element of gold demand, while eliminating "official

sector sales" as a negative supply factor.

Of course, gold will someday top, and Doug Casey believes a bubble in gold

and related equities is highly likely at some point, courtesy of the

trillions more currency units governments will create in a desperate (and

ultimately unsuccessful) attempt to stave off the Greater Depression.

But we're nowhere near that point.

There's a long way to go before we start

legitimately using the "B word" (bubble) or "S word" (sell).

In the meantime, I suggest using the "B word" (buy) or "A word" (accumulate)

to make your decisions about gold. This trend shift by central banks around

the world is just one of several indicators that the global economy is

increasingly politicized.

For investors, this means that extra diligence

and agility are needed, in order to avoid getting crushed by these changes.

Note: The upcoming Casey

Research/Sprott Inc. conference, Navigating the Politicized Economy, is

designed to help investors learn about developing trends and take advantage

of them not just to be protected, but to profit from the opportunities that

will present themselves. With distinguished speakers including G. Edward

Griffin (author of

The Creature from Jekyll Island), David

Walker (former US Comptroller General), and legendary resource speculator

Rick Rule.