|

could transform the power landscape. The implications are profound.

Major players in Asia, Europe, and the United States are all scaling up lithium-ion manufacturing to serve EV and other power applications.

No surprise, then, that battery-pack costs are down to less than $230 per kilowatt-hour in 2016, compared with almost $1,000 per kilowatt-hour in 2010.

McKinsey research has found that storage is already economical for many commercial customers to reduce their peak consumption levels.

At today's lower prices, storage is starting to play a broader role in energy markets, moving from niche uses such as grid balancing to broader ones such as replacing conventional power generators for reliability, 1 providing power-quality services, and supporting renewables integration.

Further, given regulatory changes to pare back incentives for solar in many markets, the idea of combining solar with storage to enable households to make and consume their own power on demand, instead of exporting power to the grid, is beginning to be an attractive opportunity for customers (sometimes referred to as partial grid defection).

We believe these markets will continue to expand, creating a significant challenge for utilities faced with flat or declining customer demand.

Eventually, combining solar with storage and a small electrical generator (known as full grid defection) will make economic sense - in a matter of years, not decades, for some customers in high-cost markets.

In this article we consider, as these trends play out, how storage could transform the operations of grids and power markets, the ways that customers consume and produce power, and the roles of utilities and third parties.

Our analysis is directed mostly at developments in Europe and the United States; the evolution of storage could and probably will take a different course in other markets.

Implications for the utility industry

Storage can be deployed both on the grid and at an individual consumer's home or business.

A complex technology, its economics are shaped by customer type, location, grid needs, regulations, customer load shape, rate structure, and nature of the application.

It is also uniquely flexible in its ability to stack value streams and change its dispatch to serve different needs over the course of a year or even an hour.

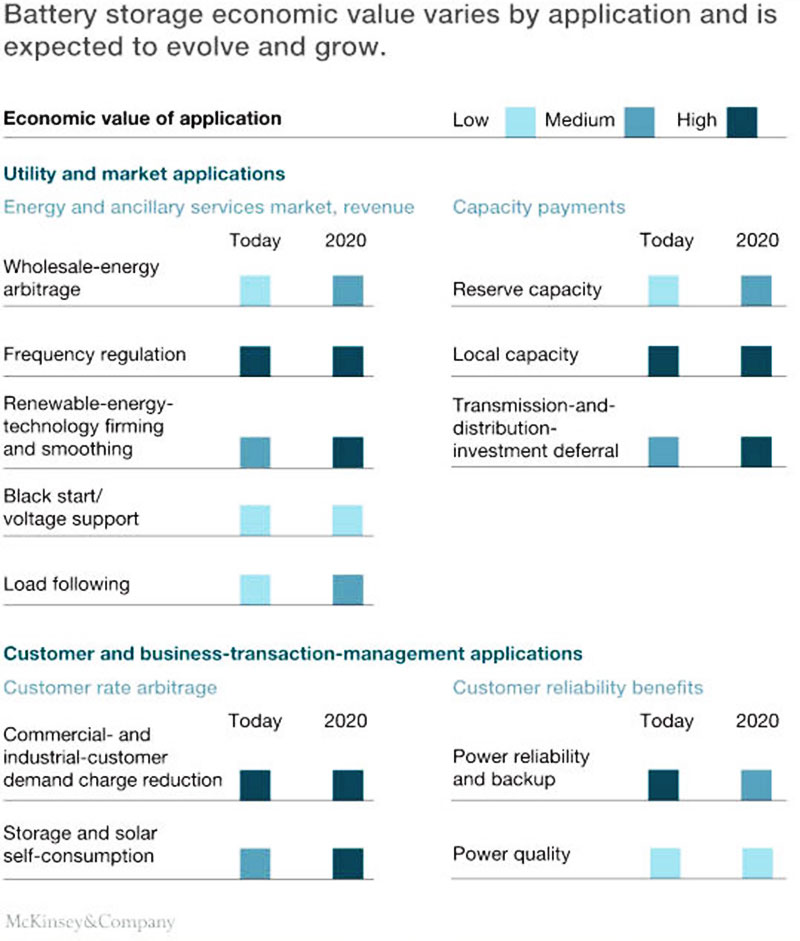

These value streams are growing both in value and in market scale (Exhibit 1).

Exhibit 1

Cheap battery storage will pose a challenge for utilities behind the meter (that is, small-scale installations located on-site, such as in a home or business).

But it will also present an opportunity for those in front of the meter (large-scale installations used by utilities for a variety of on-grid applications).

Behind the meter

Cheap solar is already proving a challenge to business as usual for utilities in some markets.

But cheap storage will be even more disruptive because different combinations of storage and solar will likely be able to arbitrage any variable rate design that utilities create.

Specifically, net energy metering (NEM) refers to rules that allow excess power to be sold back to the grid at retail rates; and feed-in tariffs, which are guaranteed price adders for renewable power, have played an important role in expanding the global market for renewables.

In the US states that have implemented such rules, NEM has proved to be a powerful incentive for consumers to install solar panels.

Although it has been helpful for solar, NEM also has put utilities under pressure. It reduces demand because consumers make their own energy; that increases rates for the rest, as there are fewer bill payors to cover the fixed investment in the grid, which still provides backup reliability for the solar customers.

The solar customers are paying for their own energy but not paying for the full reliability of being connected to the grid.

The utilities' response has been to design rates that reduce the incentive to install solar by moving to time-of-use pricing structures, implementing demand charges, or trying to reduce how much they pay customers for the electricity they produce that is exported to the grid.

However, in a low-cost storage environment, these rate structures are unlikely to be effective at mitigating load losses.

This is because adding storage allows customers to shift solar generation away from exports to cover more of their own electricity needs; as a result, they continue to receive close to the full retail value of their solar generation.

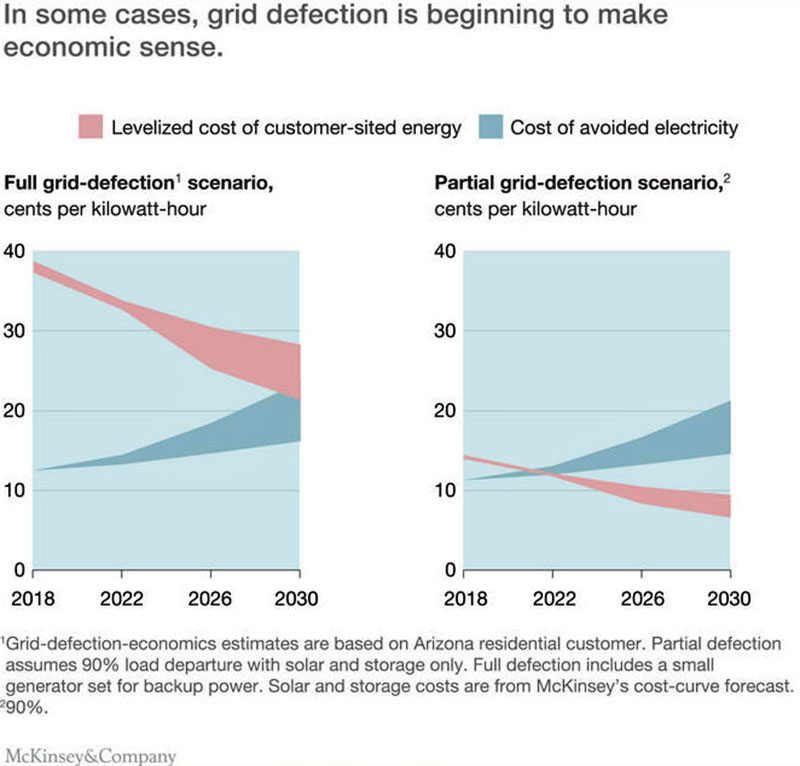

This presents a risk for widespread partial grid defection, in which customers choose to stay connected to the grid in order to have access to 24/7 reliability, but generate 80 to 90 percent of their own energy and use storage to optimize their solar for their own consumption.

We are already seeing this begin to play out in places where electricity costs are high and solar is widely available, such as Australia and Hawaii.

On the horizon, it could occur in other solar-friendly markets, such as Arizona, California, Nevada, and New York (Exhibit 2 below).

Many utility executives and industry experts thought the risk of load loss was overblown in the context of solar; the combination of solar plus storage, however, makes it much more difficult to defend against.

Exhibit 2

Full grid defection - that is, completely disconnecting from the centralized electric-power system - is not economical today.

At current rates of cost declines, however, it may make sense in some markets earlier than anyone now expects. Of course, economics alone will not dictate how much and when customers choose to disconnect from their utilities.

For example, another important factor is confidence in the reliability of their on-site power.

But this dynamic will affect business-model and regulatory decisions sooner.

In front of the meter

Storage can also benefit utilities by helping them to address the challenges of planning and operating the grid in markets where loads are expected to be flat or falling.

Regulators in some US states, for example, are testing new models of compensation by offering utilities incentives to earn returns by providing contracts for distributed generation.

This would, among other things, allow utilities to defer expensive new investments and reduce the risk of long-lived capital projects not being used.

Utilities are also acting to procure storage assets to address both long-term regulatory requirements and short-term needs, such as reliability and deferring the construction of a new substation.

As storage costs drop, such projects could lower generating costs - and, thus, consumer electricity rates - by putting further pressure on existing conventional gas and coal-generation fleets, depressing prices in capacity markets and providing load-following services.

What utilities can do

Utilities must start now to understand how low-cost storage is changing the future. In effect, utilities need to disrupt themselves - or others will do it for them.

There are two broad categories of action to consider.

The role of third parties

As for third parties - meaning distributed-energy-resource (DER) companies, technology manufacturers, and finance players - there is tremendous potential for growth. But they must be nimble to take advantage of these opportunities.

Distributed-energy-resource companies can devise new combinations of solar and storage, tailored to specific uses.

While storage could eventually provide more customer value and lower bills, new rate structures will be more complex and policy is unlikely to lock in rates for long periods.

But shorter periods of defined rates and more complex rate schedules will make it more difficult for DER providers to add new customers, who don't like complexity and want to be sure their investment will pay off.

New product offerings and financing creativity could solve these challenges and tempt customers currently sitting on the fence.

Technology players will need to understand how and where to play along the storage value chain, and adapt their offerings to meet customer needs as the technology and use cases quickly evolve.

Financing players, such as banks and institutional investors, will need to create options that adapt and match the investment horizon of the customer.

As the market grows more confident of the underlying economics and performance of storage, they will develop financial products adapted to the technology's specific needs.

When that happens, financing costs will fall, further expanding the market's potential, creating a virtuous cycle akin to what has happened to solar this past decade.

***

Battery storage is entering a dynamic and uncertain period.

There will be big winners and losers, and the sources of value will constantly evolve depending on four factors:

All this will be treacherous territory to navigate, and there will no doubt be missteps along the way.

But there is also no doubt that storage's time is coming...

|