|

When it comes to firmly established, currency-for-commodity, self reinforcing systems in the past century of human history, nothing comes close to the petrodollar:

But that is the past, and with rapid changes in modern technology and extraction efficiency, leading to such offshoots are renewable and shale, the days of the petrodollar "as defined" may be over.

So what new trade regime may be the dominant one for the next several decades?

According to some, for now mostly overheard whispering in the hallways, the primary commodity imbalance that will shape the face of global trade in the coming years is not that of energy, but that of food, driven by constantly rising food prices due to a fragmented supply-side unable to catch up with increasing demand, one in which China will play a dominant role but not due to its commodity extraction and/or processing supremacy, but the contrary:

But first, some perspectives from Karim Bitar on CEO of Genus, on what is sure to be the biggest marginal player of the agri-dollar revolution, China, whose attempt to redefine itself as a consumption-driven superpower will fail epically and very violently, unless it is able to find a way to feed its massive, rising middle class in a cheap and efficient manner.

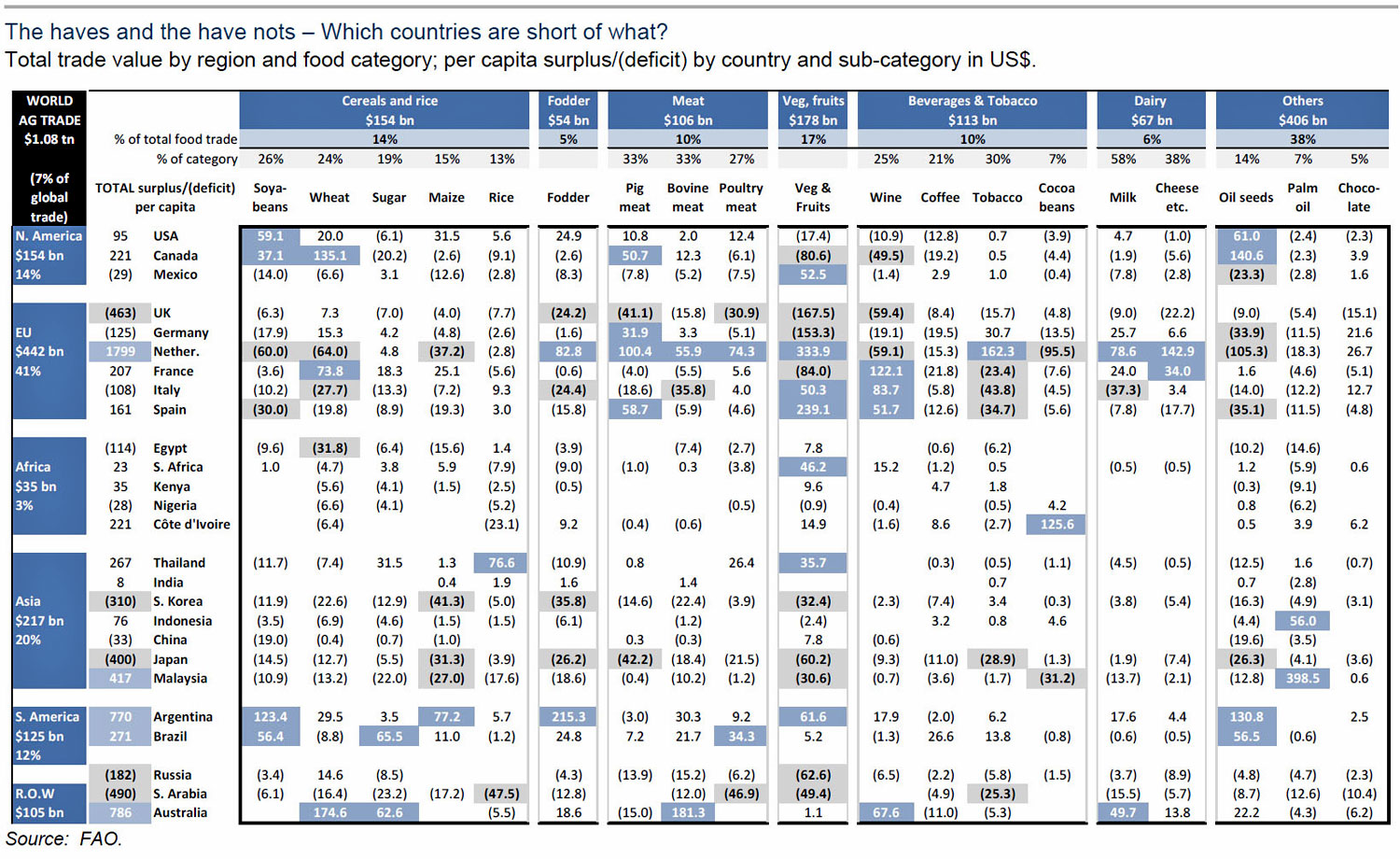

But before that even, take note of the following chart which takes all you know about global trade surplus and deficit when narrowed down to what may soon be that all important agricultural (hence food) category, and flips it around on its head.

Karim Bitar on China:

The problem for China, and to a lesser extent India, however one defines it, is that it will need increasingly more food, processed with ever greater efficiency for the current conservative regime to be able to preserve the status quo, all else equal.

And for a suddenly very food trade deficit-vulnerable China, it means that the biggest winners may be Brazil, the US and Canada. Oh and Africa. The only question is how China will adapt in a new world in which it finds itself in an odd position: a competitive trade disadvantage, especially its primary nemesis: the USA.

So for those curious how a world may look like under "the Agri-dollar," read on for some timely views from GS' Hugo Scott-Gall.

Meaty problems, simmering solutions

What potential impacts could a further re-pricing of food have on the world? Why might food re-price?

Because demand is set to rise faster than supply can respond. The forces pushing demand higher are well known, population growth, urbanization and changing middle class size and tastes. In terms of economic evolution, the food price surge comes after the energy price surge, as industrialization segues into consumption growth (high-income countries consume about 30% more calories than low income nations, but the difference in value is about eight times).

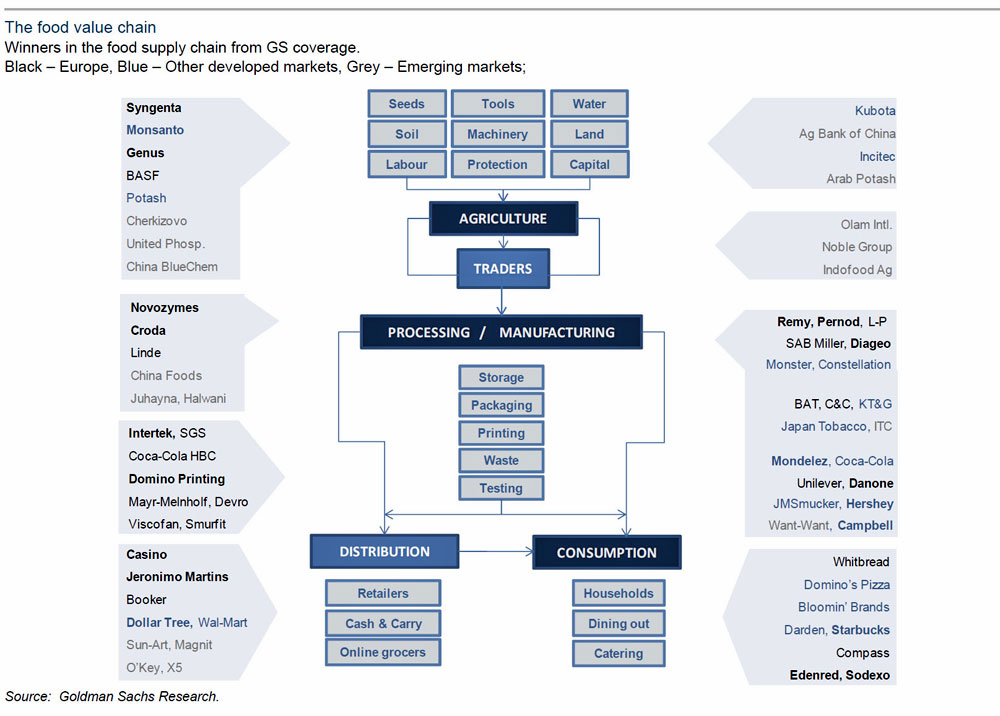

Here, we are keenly interested in how the supply side can respond, both in terms of where and how solutions are found, and who is supplying them.

We are drawn towards an analogy with the energy industry here:

The key question for us is, can and will something similar happen in food?

It’s hard to argue that the ingredients that sparked energy’s supply-side response are all present in the food supply chain. In food, there’s huge fragmentation, a lack of coordination, shortages of capital in support industries (infrastructure) and only pockets of isolated innovation. We suspect that the supply-side response may well remain uncoordinated and slower than in other industries.

But things are changing. Those who disagree with Thomas Malthus will always back human ingenuity.

As well as looking at where the innovators in the supply chain are (from page 10), and where there are sustainably high returns through IP (e.g., seeds, enzymes etc.), we need to think about the macro and micro economic impacts of higher food prices, and soberingly, the geo-political ones.

Slimming down

Could the demand destruction that higher energy prices have precipitated occur in food?

There are some important differences between the two that make resolving food imbalances tougher. Food consumption is very fragmented and there is less scope for substitution.

Changing eating habits is much harder than changing the fuel burnt for power.

And, ultimately, food spend is less discretionary that energy, i.e., the scope for efficient consumption is more limited and consumers will not (and cannot) voluntarily delay consumption, let alone structurally reduce it.

This means that higher food prices, especially in economies where food is a greater portion of household spending, will lead to either lower consumption of discretionary items or a reduced ability to service debt (with consequent effects on asset prices). When oil prices spiked in the late 1970s, US consumers spent c.9% of their income on energy vs. an average of 7% over the previous decade.

And yet, the total savings rate rose by c.2% as they overcompensated on spending cuts on other items. 2007-09 saw a similar phenomenon too.

Even the most cursory browse through history shows that high food costs can act as a political tinderbox (so too high youth unemployment), and we believe there is a degree of overconfidence with regard to the economic impact of food prices in the West: food costs relative to incomes may look manageable, but when there is no buffer (i.e., a minimal savings rate) then there are problems.

Food spend as a percentage of total household consumption expenditure is a relatively benign 14% in the US, versus c.20% for most major European nations and Japan. This rises to c.40% for China and 45% for India. Of course, as wages rise, the proportion of food within total consumption expenditure falls, but that is only after consumption hits a ceiling.

Currently, India and China consume about 2,300 and 2,900 calories per capita per day, compared to a DM average of about 3,400. If the two countries eat like the West, then food production must rise by 12%.

And if the rest of the world catches up to these levels then that number is north of 50%.

The scramble for Africa’s eggs

In terms of ownership of resources, food, like energy, can be broken into haves and have-nots.

While there are countries that have been successful without resources, it is quite clear that inheriting advantages (in this case good soil, climate and water) makes life easier. But that, of course, is only half the battle; what is also required is organization, capital, education and collaboration to make it happen.

Take Africa. It has 60% of the world’s uncultivated land, enviable demographics and lots of water (though not evenly distributed). Basic infrastructure, consolidation of agricultural land and minimal use of fertilizers and crop protection could do wonders for agricultural output in the region. But that’s easier said than done.

Several African economies also need better access to information, education, property rights and access to markets and capital.

Put another way, it needs better institutions. If Africa does deliver over the coming decades, rising food prices will alter the economics of investing in the region. The next scramble for Africa should be about food (while it is about hard commodities now and in the late 19th century it was about empire size).

Fertilizer consumption has a diminishing incremental impact on yields, but Africa (along with several developing economies elsewhere) is far from touching that ceiling. Currently, Africa accounts for just 3% of global agricultural trade, with South Africa and Côte d'Ivoire together accounting for a third of the entire continent’s exports.

But if the world wants to feed itself then it needs Africa to emerge as an agricultural powerhouse.

Higher up the production curve is China, which has been industrializing its agriculture as it seeks to move towards self sufficiency.

Power consumed by agricultural machinery has almost doubled over the last decade, while the number of tractors per household has tripled, driving per hectare output up by an average of more than 20% over the same period.

Even so, in just the last 10 years China has gone from surplus to deficit in several meat, vegetable and cereal categories. So a lot more needs to be done, and a shortage of water could also prove to be an impediment, especially in some of its remote areas.

The power of the pampas

With significant surpluses in soybeans, maize, meat and oilseeds, Brazil and Argentina have led the Latin American continent in terms of food trade.

Current surpluses are 6x and 3x 2000 levels, versus only a 30% increase in the previous decade, and are rising. A key impediment to boosting exports is infrastructure. Food has to travel a long way just to reach the port, and then further still to reach other markets.

Forty days is possibly acceptable for iron ore to reach China on a ship from Brazil, but that would prevent several perishable food items from being exported.

And hence, solution providers in terms of durability, packaging, refrigeration and processing will be in demand. Also, while you could attribute a lot of the agricultural success of LatAm economies to good conditions, they have also benefitted from the adoption of agricultural innovation.

For instance, more than a third of crops planted in the region are as seeds that are genetically modified, versus more than 45% in the US and about 12% in Asia.

Genetically modified crops are not new. They provide solutions to some of the most frequent constraints on agricultural yields (resistance to environmental challenges including drought and more efficient absorption of soil nutrients, fertilizers and water) or add value by enhancing nutrient composition or the shelf life of the crop.

And while the adoption of GM crops and seeds is far from wholehearted, particularly in Europe, it’s most certainly a key part of the 'solution' in economies that are set to face a more severe food shortage.

The last mango in Paris?

Europe’s deficit/surplus makes for interesting reading. Seventeen of the 27 EU countries face a food trade deficit, and yet, the EU overall recorded a surplus (barely) in 2010 for only the second time in the last 50 years (see chart).

Broken down further, the UK is the largest food importer, followed by Germany and Italy, while the Netherlands and France lead exports thanks to their very large processing industries.

If Europe’s future is one of relative economic decline, then reduced purchasing power when bidding for scarce food resources is an unappetizing prospect.

Therefore, it needs all the innovative solutions it can muster, or import substitution will have to increase. It’s important to note that being in overall surplus or deficit can mask variety at the category level, i.e., Europe is a net importer of beef, fruit & vegetables, and corn, while its exports are helped by alcohol and wine specifically.

Japan, in particular, is very challenged. It is the only country in the preceding table to show a deficit in every single food category.

We conclude our trip around the world in North America. Large-scale production, access to markets, a home to innovation and favorable regulation has meant that the US (and Canada) continues to dominate some of the key agricultural resources such as soybeans, corn, fodder, wheat and oilseeds.

Put this self sufficiency together with the medium-term potential for energy self sufficiency and relatively good demographics (better than China), and a rosier prognosis for the US, versus the rest of the Western world and parts of Asia, begins to fall into place.

Agri-dollars on the rise

Before we conclude, we need to devote a few lines to the geo-political and macro economic consequences of higher food prices.

It’s likely that countries will act increasingly strategically to secure food supply, and that protections (e.g., high export tariffs) may well rise. It is also likely that there are special bi-lateral deals to access stable and secure food supply.

This could obviously damage the integrity of the WTO-sponsored system. Another consequence might be the emergence of agri-dollars, in the same way that petro-dollars emerged in the 1970s. This may seem far fetched (the value of the world’s energy exports is US$2.3 tn compared to US$1.08 tn for agriculture) but it’s important to think through the consequences.

The big exporters, especially those with the scope to grow their output, may well have sustainable surpluses that can be reinvested into their economies (or extracted by a narrow part of society).

Similarly, the consequence of being a net importer will be an effective tax on consumption: disposable income in the US would jump if oil was US$25/bbl.

As we have said, we would expect the big gainers of a meaningful rise in food prices in real terms to be Brazil, the US and Canada, while Japan, South Korea and the UK would face challenges.

The top chart is important: look how China’s surplus has turned to deficit. What will happen if the Chinese middle class swells as it is expected to? And that’s the rub; what we have been used to in terms of food’s importance is set to change.

How food moves around the world is likely to change, and the flow of currency around the world will also likely be impacted.

|